When AI Startups Skip Growth and Go Straight to Glory

Last week’s Playbook Kickoff touched on this valuation frenzy—this deep dive unpacks the mechanics behind it.

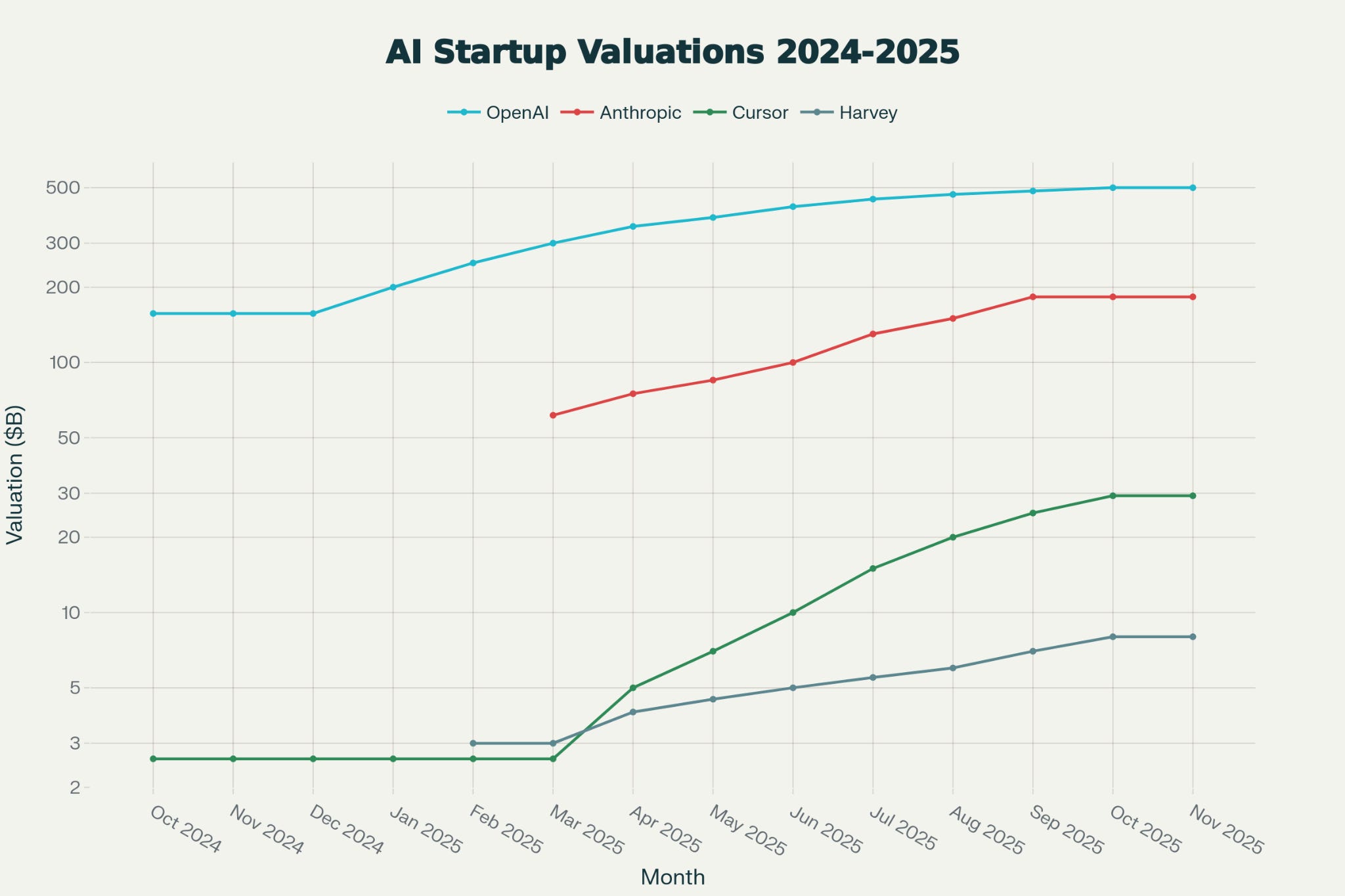

Imagine watching a company add roughly $1 billion to its paper value every single day. Sounds like fantasy? Between October 2024 and October 2025, that’s essentially what happened to one household name in the AI world. What began as a trickle of excitement turned into a full-on valuation stampede: startups raising back-to-back rounds, prices leaping overnight, and the market collectively deciding that certain plays were now worth grabbing—fast, loudly, and with very little patience for nuance.

This piece isn’t a spreadsheet parade. It’s a stroll through the causes, the consequences, and the uncomfortable choices companies must now make—framed as a story because when valuations move this quickly, narrative beats matter as much as financial ones.

What changed (and why it feels different this time)

2021 felt like a love affair with ideas: great slides, bold visions, and a generous global risk appetite. The 2024–25 sprint looks more like a marriage—messy, expensive, and with real children (read: revenue and product traction). The difference is not just capital; it’s capital meeting demonstrable demand. Customer adoption moved from experiments and pilots to real production; enterprises stopped asking “if” and started asking “how fast.” When billions in corporate capex and hyperscaler commitments meet startups that can actually show usage and recurring revenue, prices stop being theoretical.

Layer on top of that a tight compute market—an industry uniquely vulnerable to supply shocks—and you get artificial scarcity turned into pricing power. GPUs and HBM became the new scarce oil. The startups that could access capacity, credits, or partnerships suddenly found their valuations reflecting not only their software but also their access to the literal fuel of modern AI.

The new rules of the game

There are a few simple, brutal mechanics at play.

First, the “flight to quality” among investors: the pool of capital didn’t so much grow as it concentrated. VCs and crossover funds started piling into fewer names, and that concentration alone lifts prices—because everyone wants a seat at the table of the perceived winners.

Second, fundraising velocity compressed. What used to be an 18–24 month leap from Series A to B shrank to a matter of months for top-tier companies. Terms were signed quickly, rounds stacked rapidly, and the option value on “becoming the next big frontier AI” trumped the slow grind of classical due diligence.

Third, the revenue reality is, in part, real: several vertical AI plays moved from zero to meaningful ARR in record time. That made the multiples look less like irrational exuberance and more like the market repricing a new kind of growth engine—one that threads product-market fit with platform effects and enterprise stickiness.

The risks hiding behind the champagne

If you’re dazzled by meteoric multiples, good—because that’s exactly the emotional state the market feeds on. But there are structural tensions. Compute concentration means a single vendor’s allocation decisions can reshape the landscape. Talent is another choke point: elite researchers command compensation packages that only the hyperscalers can sustain. Meanwhile, many mid-tier startups are carrying burn rates that assume perpetual access to capital. That’s a fragile assumption.

And then there’s the regulatory and geopolitical shadow: export controls, policy reversals, and sovereign funds shifting strategic priorities can rewire investor appetites overnight. In short: a quality boom sits atop a thin financial crust—real adoption below, and speculative heat above.

What this means for the rest of the economy (and why it matters to you)

Non-AI companies face a stark strategic fork. Build and burn—try to assemble elite teams, buy compute, and hope for a breakthrough—or become smart integrators, leveraging external capabilities to accelerate impact. For many organisations, the math doesn’t add up: hiring elite researchers, provisioning GPU-heavy infrastructure, and sustaining long R&D timelines is a losing game unless you’re prepared to become a frontier AI shop.

That’s where a quieter story is unfolding: AI-enabled operational partnerships. Companies that help other businesses adopt and deploy AI—without forcing them to become full-time AI shops—are gaining traction. They stitch together APIs, fine-tuning, deployment pipelines, and governance so firms can capture AI upside while avoiding the full capital and talent burden. Mentioning this isn’t a pitch; it’s a recognition of market logic. Platforms that bundle AI talent, tools, and delivery—allowing firms to hedge their bets—will win a steady, less headline-grabbing race.

If you’re curious about pragmatic, delivery-first approaches that balance speed with governance, we are combining AI talent, operational workflows, and performance-linked delivery to help companies move quickly without blowing up budgets—an approach worth exploring if you’re not building a frontier AI shop.

A tale of three possible tomorrows

The future will be a function of supply, regulatory clarity, and enterprise ROI.

Path one: continued acceleration. Compute remains constrained, enterprise ROI keeps surprising on the upside, and valuations climb further for the select winners.

Path two: normalization. Supply eases, the scarcity premium fades, and mid-tier valuations retrace as rationality returns.

Path three: a sharper correction. Policy shocks or macro reversals trigger a rapid re-pricing, and many late-stage winners find themselves negotiating survival rather than celebration.

In practice the market will bifurcate. The top handful of frontier players will keep a disproportionate share of capital and talent; the rest will either settle into realistic revenue multiples or be subsumed through consolidation.

What to watch next (without turning this into a checklist)

If you care about strategy rather than spectacle, watch the plumbing: compute pricing and allocations, the first major AI IPO price-to-revenue, and whether enterprise pilots convert into demonstrable cost savings. Those signals will determine whether the frenzy was a re-rating of durable value or merely the last hurrah of a crowded trade.

Where sensible companies should position themselves

The practical move is not to chase headline valuations but to secure optionality. If you can’t justify building an in-house frontier team within a sane budget horizon, choose partners that combine AI expertise with delivery muscle. Long-term contracts, performance-linked KPIs, and vendor neutrality are your hedges.

That’s also where firms that specialise in AI-integrated talent and delivery—those that can deploy hybrid teams combining human judgment with model scale—become useful. They don’t replace strategy; they make the strategy executable without turning your balance sheet into a high-stakes bet. For companies that need rapid AI lift without the hyperscaler war chest, partnering with delivery-first specialists is a practical, capital-efficient route forward.

We’ve been working with teams that take this exact approach—helping organisations deploy AI-powered workflows while protecting runway and governance. It’s pragmatic, not glamorous. And in a boom like this, pragmatic often wins.

The final note: a quality bubble within a real boom

This market is messy and magnificent: part genuine structural shift, part speculative euphoria. The next 18–24 months will separate firms that built durable value from those that rode momentum. For executives and founders, the choice is clear—be realistic about what you can build, and be shrewd about who you partner with. The winners won’t be the loudest; they’ll be the ones who turned the AI moment into real, repeatable outcomes.

If you’re thinking about how to move fast without overcommitting capital or losing strategic focus, there’s a pragmatic middle ground: assemble AI capability through trusted delivery partners who combine talent, tools, and governance. It’s not glamorous, but in a market this volatile, pragmatic often outperforms heroic.

Aligns with my vision. Thank you for sharing @Sharique Nisar 🙌🏄♂️♾️