The Margin Machine

How AI-Enabled Outsourcing Is Quietly Restructuring Operating Leverage in 2026

Outsourcing has always been sold as a cost story. Move work offshore, compress overhead, protect margins. That logic still holds. But in 2026, it is no longer the complete picture.

The more consequential shift is structural: outsourcing is becoming an intelligence lever, not just a labour lever. AI is allowing companies to compress delivery costs, expand throughput, reduce rework, improve collections, and scale support functions without adding headcount linearly. The model is evolving from labour arbitrage to intelligence arbitrage — and the margin economics that follow are meaningfully different.

83% of surveyed executives are already leveraging AI as part of outsourced services. 20% are actively developing strategies to manage digital workers. — Deloitte Global Outsourcing Survey, 2026

That is no longer experimentation. That is operating reality. And the question in 2026 is not whether AI will affect outsourcing. It is how much margin it can structurally unlock — and which firms will capture the upside.

I. WHY 2026 IS DIFFERENT

The years 2023 and 2024 were characterised by GenAI pilots, boardroom enthusiasm, and vendor showcases. 2025 was a year of integration. 2026 is shaping up as the operating model year — the moment when AI stops being a capability experiment and starts being embedded in recurring workflows: support, finance, IT operations, back-office processing, and service delivery.

Two things are converging. First, enterprise buyers have shifted their expectations: AI is increasingly part of the delivery baseline, not a premium innovation layer. Second, actual productivity and cost benefits are still uneven. Governance structures, workflow redesign, and commercial contracting have not fully caught up.

That gap — between adoption and value capture — is where the real analytical story lives in 2026. The market is separating firms that have added AI tools from firms that have redesigned outsourced work around AI. That distinction shows up in margins.

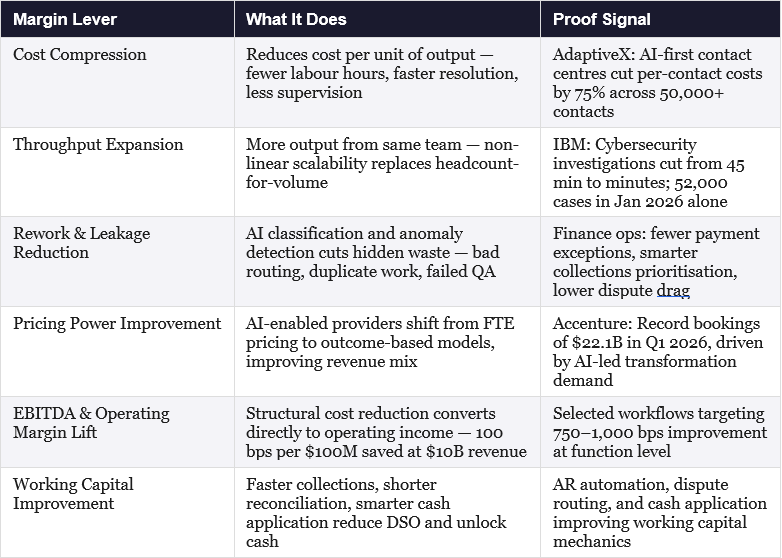

II. SIX PATHWAYS TO MARGIN EXPANSION

If you strip away the AI buzzwords, operating margin expansion through AI-enabled outsourcing is happening via six distinct economic pathways. Each is measurable. Each has real-world proof points already visible in the market.

The $10 billion illustration is worth dwelling on. A company of that scale that removes $100 million in operating cost through AI-enabled outsourcing and workflow redesign produces a 100 basis point operating margin improvement. That is not a minor tweak. That is the kind of movement that changes analyst ratings and board conversations.

The margin story is not ‘AI replaces people.’ It is: AI changes the operating leverage of outsourced functions.

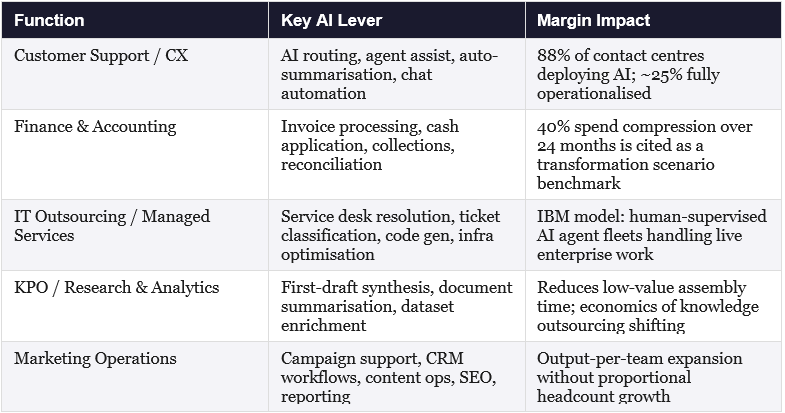

III. WHERE THE GAINS ARE SHOWING UP FIRST

Not every function is seeing the same magnitude of impact. The strongest gains in 2026 are concentrated in processes that are repetitive but not entirely rules-based, document-heavy, communication-intensive, exception-prone, and measurable.

The CX Signal Worth Watching

Customer support is particularly instructive because the data is unusually measurable. An 88% deployment rate in contact centres, combined with only ~25% full operationalisation, tells you something precise: the margin upside is real but still partially trapped behind workflow redesign and integration discipline. That gap is what will separate CX leaders from laggards in the next 12–18 months.

IV. WHY SOME FIRMS STILL FAIL TO CAPTURE THE UPSIDE

AI does not automatically create margin expansion. A significant portion of AI outsourcing initiatives are underperforming for identifiable and avoidable reasons.

▸ They automate bad processes. Fragmented or exception-heavy workflows accelerate the mess, not the output.

▸ They overestimate labour removal. Governed enterprise environments retain more human review layers than vendor ROI models assume.

▸ They ignore adoption. If teams don’t use the tools, productivity gains stay theoretical.

▸ They fail to redesign contracts. A commercial model that still rewards headcount will trap most of the AI value.

▸ They underestimate governance costs. Security, compliance, auditability, and human oversight remain non-negotiable in finance, healthcare, and regulated support.

Capita’s March 2026 results illustrate this tension with uncommon clarity. Reuters reported that roughly two-thirds of Capita’s revenue is now AI-enabled and its contract pipeline has nearly doubled to £19.8 billion — yet the company simultaneously warned of margin pressure in 2026 due to startup costs and contact centre weakness.

AI doesn’t create margin expansion because it exists in the stack. The best results come when firms redesign the workflow around AI — not the other way around.

Deloitte’s survey reinforces this. Deployment is moving faster than value capture. The percentage of executives reporting clear cost or productivity benefits remains well below the adoption rate. That delta is the operational challenge — and the competitive opportunity — of 2026.

V. THE STRUCTURAL CONCLUSION

The firms best positioned to benefit from AI-enabled outsourcing in 2026 share a common trait: they are using AI to redesign economics, not simply to add AI-themed capabilities to existing workflows.

Enterprise buyers win when they select processes genuinely suited to AI-enabled redesign, align vendors to measurable business outcomes rather than headcount savings, and track unit economics and margin — not innovation optics.

Providers win when they embed AI into delivery rather than selling it as a bolt-on, move beyond labour-led pricing models, and operationalise productivity gains at delivery scale. Accenture’s record bookings and IBM’s agent-operating-model are two very different examples of the same underlying truth: buyers are increasingly paying for AI-enabled operating leverage, not outsourced labour capacity.

2026 will likely be remembered not as the peak of this shift, but as the year the model became visible. Once AI-enabled outsourcing consistently delivers lower cost-to-serve, higher throughput, fewer errors, and better working capital, it stops being an innovation project. It becomes a competitive expectation.

And once that happens, the next strategic question becomes urgent: if AI-enabled outsourcing becomes standard, who keeps the margin upside? Some flows to enterprise buyers. Some is captured by providers. Some moves to platform and infrastructure players. But the direction is already clear.

Outsourcing is no longer about moving work to cheaper labour. It is increasingly about building smarter operating models that expand margins structurally.