The Quiet Revolution in Enterprise IT: Why 99% of C-Suite Leaders Now Outsource Critical Functions

C-suite outsourcing trends: how companies are buying scarce IT skills while cutting operating costs

In Monday’s kickoff, one idea stood out: outsourcing is now a strategic shock absorber. It lets organizations stabilize delivery during uncertainty — scaling capacity without locking in permanent cost or headcount. This deep dive explains why that’s happening, why it’s structural, and why the winners will treat outsourcing as capability sourcing, not cost cutting.

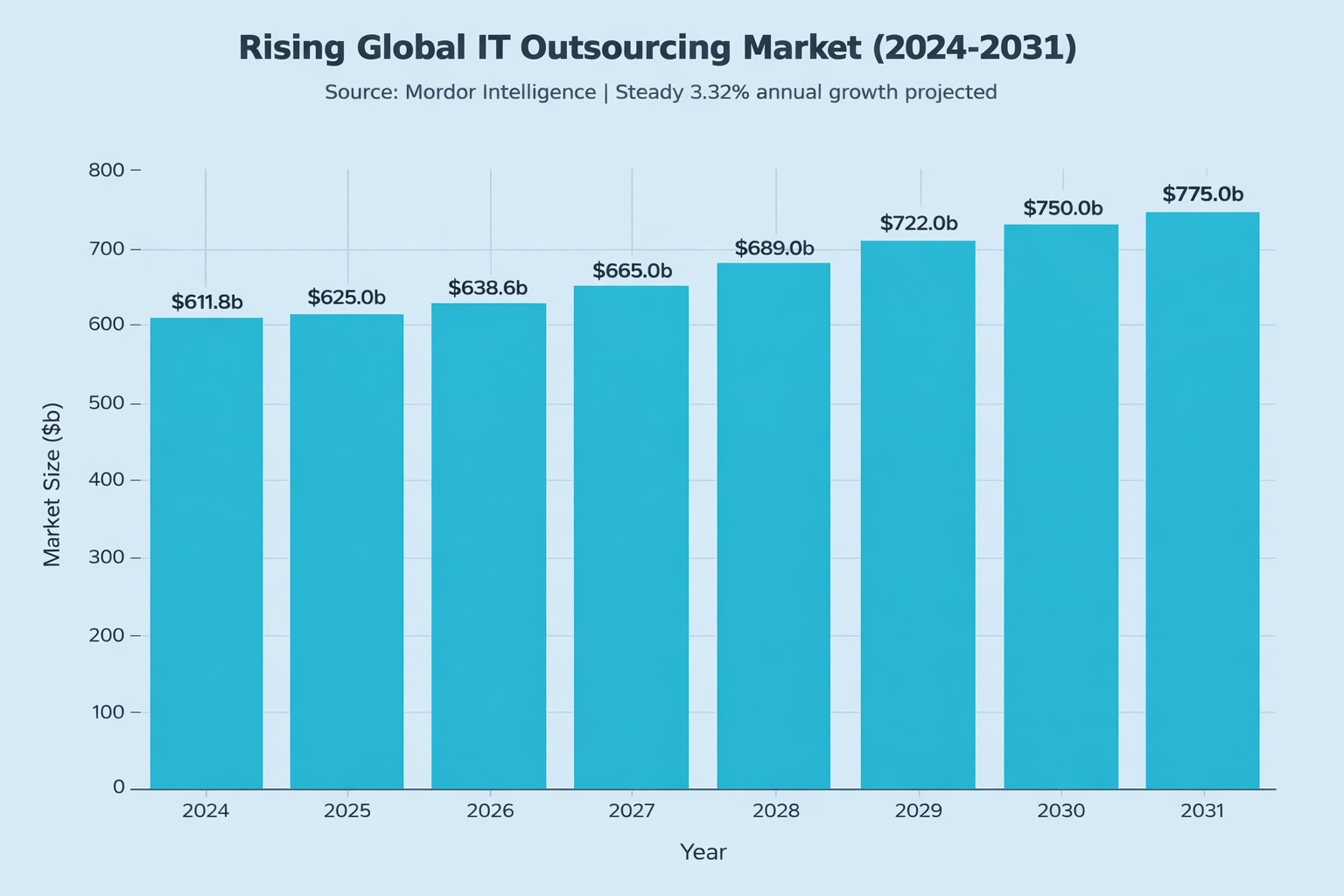

The IT outsourcing market reached $638 billion in 2026. That number matters less than what drives it.

Executives no longer outsource to reduce costs. They outsource because they cannot find talent. The shift is structural, not cyclical. Organizations that treat outsourcing as a cost-cutting exercise will fail. Those that understand it as capability sourcing will compete.

The Talent Constraint

Rimini Street surveyed 4,300+ C-suite executives. Ninety-eight percent report that IT talent shortages affect their technology vision. Sixty-eight percent describe the impact as significant.

India produces 1.5 million engineers annually and commands 17.58% of the global outsourcing market. This vast pipeline cannot satisfy demand. Fifty-seven percent of IT recruitment managers cannot find skilled staff. Thirty-six percent of C-suite leaders state that skills gaps limit growth opportunities.

The operational reality is clear: 23% of IT workforce time maintains existing ERP systems. This creates the business case. Externalize maintenance. Free internal capacity for AI implementation, cloud migration, digital transformation.

When executives identify five-year priorities, 46% select AI and automation adoption. Forty-four percent emphasize cybersecurity and risk management. Cost optimization ranks fourth at 39%. Cost has become table stakes, not competitive advantage.

Geographic Recomposition

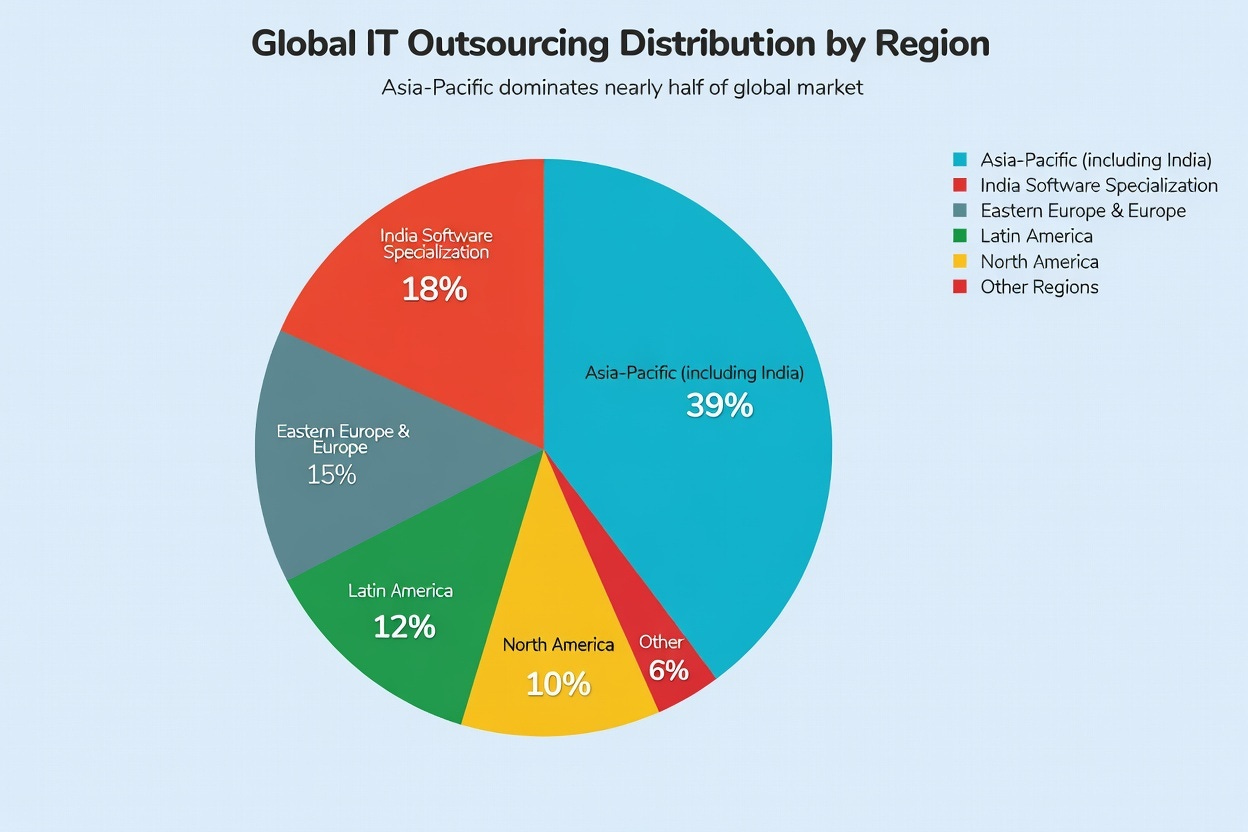

Asia-Pacific commands 36-42% of total outsourcing activity. India remains the largest single market. Latin America is growing faster.

The SSON/Auxis 2024 report documents the shift. Latin America’s share of North American outsourcing expanded from 44% in 2016 to 84% in 2024. Near-doubling in eight years.

Decision criteria have changed. India provides cost savings of 50-70% versus Western countries. Latin America provides overlapping time zones, cultural proximity, higher retention, quality consistency. Executive satisfaction with Latin American providers reaches 87%. Satisfaction with Asian providers: 53%.

Mexico produces 130,000+ qualified engineers annually. Colombia and Costa Rica have established specialized hubs for financial services and technology outsourcing.

Organizations now operate multi-region strategies. India handles transactional, high-volume functions optimized for cost. Latin America serves collaboration-intensive, time-sensitive, quality-critical work. Eastern Europe (Poland, Romania, Czech Republic) provides specialized technical expertise: blockchain, cloud-native development, cybersecurity.

Each region solves specific constraints.

Service Concentration

Organizations concentrate outsourcing investments in discrete functions. Cybersecurity and infrastructure management rank as top outsourced services for current and future investment.

Infrastructure outsourcing commands 45.05% of total market. Enterprises rely on resilient data center operations, network services, disaster recovery. The cybersecurity services market expands from $219 billion in 2025 to $566+ billion by 2032.

Organizations lacking internal capacity for 24/7/365 security operations outsource to managed security providers. IBM research quantifies the financial rationale: organizations maintaining incident response teams reduce breach costs by $2.66 million per incident.

Application development shows 72% outsourcing penetration. Application support: 69%. Emerging technologies including generative AI and blockchain: 75%.

The pattern reveals strategic hierarchization. Commodity functions (maintenance, support) versus strategic capabilities (AI implementation, application modernization).

The Vendor Lock-In Problem

Thirty-five percent of C-suite leaders cite substantial frustrations with vendor lock-in. Forced upgrades. Limited flexibility. Escalating costs.

As companies deepen relationships with major software vendors—Oracle, SAP, Salesforce—they become dependent on vendor-directed roadmaps and expensive upgrade cycles.

The financial consequences are visible. The UK Cabinet Office warned that overreliance on AWS could expose government institutions to costs exceeding £894 million. Microsoft faced antitrust penalties of $1.12 billion after licensing practices discouraged customer cloud migration. VMware customers experienced price increases up to 1,000%, combined with operational disruptions from deeply integrated systems.

Forward-thinking organizations respond with multi-layered strategies:

Outcome-based contracts tying vendor compensation to business results

Cloud-native, microservices architectures reducing vendor dependency

Explicit contractual data portability protections

Multi-vendor strategies preventing single-vendor concentration

These approaches increase short-term operational complexity. They provide long-term flexibility and competitive advantage.

Agentic AI: The Next Wave

Gartner projects 40% of enterprise applications will incorporate agentic AI by 2026. Up from less than 5% today.

This represents a shift from software that waits for human instruction to software that autonomously observes, decides, acts.

Organizations unprepared to implement agentic AI at scale face competitive disadvantage. Few possess internal expertise to design and operationalize these systems. This capability gap drives a new outsourcing wave focused not on labor arbitrage but on specialized AI implementation expertise.

Major ERP vendors—Oracle, IFS, SAP—are embedding agentic AI agents directly into their platforms.

Accounts payable outsourcing exemplifies the evolution. Modern agentic approaches employ AI agents to autonomously perform invoice capture, vendor matching, fraud detection, approval routing. Human handlers focus exclusively on edge cases. Organizations implementing this model achieve 25-30% cost reductions per invoice while improving compliance.

Market Trajectory

The global IT outsourcing market will expand to $750+ billion by 2030. The broader IT services outsourcing ecosystem will exceed $1 trillion.

The composition will shift:

AI will constitute 20-30% of outsourcing budgets by 2030, up from negligible amounts today

Nearshore outsourcing will increase from 15-20% toward 30-35% of total activity

Outcome-based pricing will expand from niche toward mainstream

Infrastructure-as-a-Service will grow as organizations prefer operational expense models to capital-heavy infrastructure ownership

What This Means Operationally

Strategic level: Reframe outsourcing as strategic capability sourcing rather than cost reduction. Define priorities based on capability gaps and competitive differentiation, not labor arbitrage. Develop multi-region strategies combining offshore cost advantages, nearshore collaboration benefits, specialized expertise hubs.

Program level: Prioritize outcome-based contracts tying vendor compensation to measurable business results. Implement hybrid delivery models combining strategic internal functions with operational outsourcing. Maintain technical governance onshore or nearshore to oversee offshore execution.

Vendor selection: Prioritize partner stability and technical expertise depth over cost competitiveness. Negotiate explicit contractual protections including data portability, staged exit plans, change-of-control provisions. Conduct periodic “switching feasibility” exercises validating ability to transition work to alternative vendors.

The Reframe

Outsourcing has transformed from cost-optimization mechanism to strategic capability-sourcing engine. Driven by acute talent scarcity, AI imperatives, organizational pressure for accelerated innovation delivery.

Ninety-nine percent of C-suite organizations now operate outsourcing as a core model.

Geographic composition shifts in real time. Latin America emerges as nearshore alternative to India. Organizational focus shifts from cost reduction to value creation. AI implementation, cybersecurity, infrastructure management represent priority investment areas.

The tension between specialization benefits and vendor lock-in risks requires proactive mitigation. Outcome-based contracts. Architectural independence. Multi-vendor strategies.

Organizations that implement outsourcing strategically—aligned with organizational capabilities, partner selection, contractual governance—will access substantial competitive advantage. Those treating outsourcing as commoditized cost reduction will face vendor dysfunction and escalating total costs.

The question is not whether to outsource. The question is how to do so strategically.

If you’re reviewing your current outsourcing setup (or building one), and want a partner that can take ownership of execution while your internal team stays focused on core priorities, Market Quotient can help. Happy to share examples of delivery models, timelines, and what governance looks like in practice.